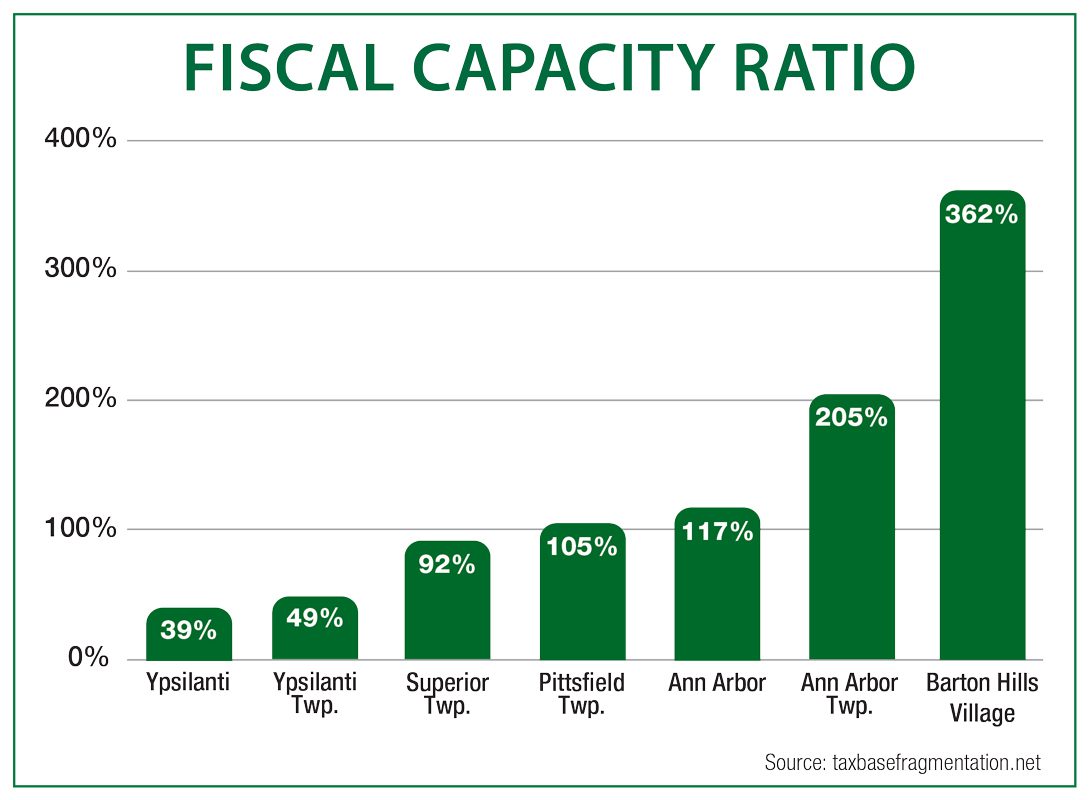

The city and township of Ann Arbor have a relatively privileged tax base position compared to their neighbors. Barton Hills Village’s FCR of 362 percent makes it a municipal tax haven.

The study, coauthored by U-M sociology professor Robert Allen Manduca and published in Oxford University’s Socio-Economic Review explores what it calls tax base fragmentation. It’s based on a simple concept: some jurisdictions have higher property values than others—even some right next door—which translates to more property tax revenue. In turn, these privileged jurisdictions have more funding for public services like police, education, public transit, and parks, recreation, and natural area preservation, as well as the flexibility of offering a lower property tax rate than would otherwise be possible.

Manduca and his colleagues’ research establishes a method to precisely quantify tax base fragmentation. This could in turn help researchers and policymakers better understand the cascading consequences when one town doesn’t have enough tax revenue to meet the needs of its people while nearby ones do.

So, how do these findings play out here?

It may come as no surprise that Ann Arbor has a relatively privileged tax base position compared to other parts of the county. The city scores high on the Fiscal Capacity Ratio (FCR) that Manduca and his colleagues have developed, which measures underlying tax base potential—that is, the total appraised value of all taxable property divided by the number of people living there. With the FCR, Manduca says, “we’re measuring the disparity in the tax base” between different cities within the metro area. Put simply, the higher the FCR, the more money the jurisdiction has available.

Ann Arbor has a 117 percent FCR, and for Ann Arbor Twp., that number is 205 percent. But right next door, Ypsilanti has a 39 percent FCR, and Ypsi Twp., 49 percent.

Ypsilanti City Manager Andrew Hellenga says that tax base fragmentation finally gives a definition to a phenomenon that he has had to grapple with.

“The poverty of the county is essentially concentrated in this area,” says Hellenga. Because of EMU, “a third of the city is tax-exempt. Also, state transfers have been decreasing since the nineties. So we have to do more with the revenue that we’re able to bring into the city for proper functions.”

According to the study, tax base fragmentation arises from the system of government here in the United States—which differs from other advanced democracies where municipalities are funded through transfers from federal and regional governments.

“Local governments in the U.S. are so dependent on revenue that’s generated locally, as opposed to transfers from other levels of government. That really creates incentives for this sort of pattern to get perpetuated,” Manduca continues. “Because it’s possible to move across a jurisdictional boundary, especially if you’re wealthy, to then pay a much lower tax rate just because you’re living on one side of a line, that really incentivizes people with the means to do this and exacerbates some of the inequalities that we see.”

When a jurisdiction’s tax base is more than three times the average of the surrounding metropolitan area—an FCR above 300 percent—it becomes what Manduca and his colleagues term a “municipal tax haven.”

“A municipal tax haven is still part of the U.S., so it doesn’t allow its residents to avoid paying income or other taxes,” Manduca says. “But in terms of property taxes, its function is sort of similar: because it is a separate jurisdiction, its tax base is not shared with the rest of the metropolitan area, often allowing its residents to pay much lower property tax rates than they would in nearby jurisdictions.”

Within Southeast Michigan, Detroit gets a 31 percent FCR, Berkley gets a 123 percent FCR, and West Bloomfield gets a 176 percent FCR. By the measure of the study, that makes these well-off suburbs, not municipal tax havens.

But Metro Detroit’s Lake Angelus is a different story. The community of 287 people in Oakland County has an FCR of 861 percent. Washtenaw County has just one municipal tax haven: Barton Hills Village, with an FCR of 362 percent.

Barton Hills leadership didn’t respond to interview requests, nor did Ann Arbor Twp. An interview with Ypsilanti Twp. leadership couldn’t be arranged.

One way to address tax base fragmentation is through revenue sharing—that is, when a state shares a portion of sales tax with local governments. This is already a practice in Michigan.

“State revenue share has a statutory component and a constitutional component,” explains Ann Arbor Mayor Christopher Taylor. “We tend to always get the constitutional revenue sharing. There is a very material delta between what we actually get for state statutory revenue sharing and what the promise would have delivered to us.”

That promise was a 1998 amendment to adopt a more equitable method of revenue sharing based on a formula that would give a higher proportion of money to jurisdictions with lower FCRs. Four years later, the formula was rescinded, resulting in widespread budget cuts throughout underfunded communities. It wasn’t until 2025 that state lawmakers restored the formula.

Flashback: A Taxing Question (Apr. 2011)

Best Practices or Budget Cuts? (Oct. 2011)

Constitutional sharing—15 percent of 4 percent of the state sales tax, distributed on a per capita basis—has been more consistent throughout the years. But FY2026 saw a $63.2 million reduction in revenue sharing due to the removal of state sales tax from gasoline and diesel.

In FY2026, Ann Arbor is projected to receive $13 million from constitutional sharing and $2.3 million from statutory sharing; in Ann Arbor Twp., those numbers are $460,092 and $2,490, respectively. The City of Ypsilanti, on the other hand, is projected to receive $2.2 million from constitutional sharing and $1.3 million from statutory sharing; Ypsilanti Twp. should receive $5.9 million and $750,582, respectively. Barton Hills is projected to receive $33,368 in constitutional sharing and a mere $187 in statutory sharing.

Tax base fragmentation is a new concept, and Manduca and his colleagues are planning to continue their research, including examining the consequences for residents’ microeconomic life. Hellenga says the most useful information for city managers and lawmakers would be studies that “shine more light” on the phenomenon and its effects, as well as the need for tax and economic equity.